Ethereum: Is Lido (LDO) Doomed To Repeat Three Arrows Capital’s Fate?

Market research firm Kaiko has published a study on the flagship protocol of Ethereum, Lido Finance (LDO). The study is a must-read for every ETH and LDO investor!

Cautionary tales serve as a valuable reminder of the risks and pitfalls that can await even the most promising projects. Remarkably, Lido Finance has embarked on a massive growth trajectory in recent months, reminiscent of former crypto industry poster child Three Arrows Capital (3AC). Riyad Carey, analyst at Kaiko, writes:

Essentially, 3AC made a bet that GBTC – a fundamentally different asset than BTC, with significant frictions in entrance and exit – would closely track BTC’s price. This saga has been front of mind as I’ve observed stETH (and other liquid staking derivatives) begin to displace ETH in DeFi protocols.

Research Findings By Kaiko

The in-depth research conducted by Kaiko offers critical insights into Lido’s operations and the potential risks it faces. According to Kaiko’s analysis, “Lido’s success story raises concerns about potential vulnerabilities and risks lurking beneath the surface.” By examining a wealth of data, Kaiko sheds light on liquidity challenges, leverage risks, and the potential for a large liquidation event.

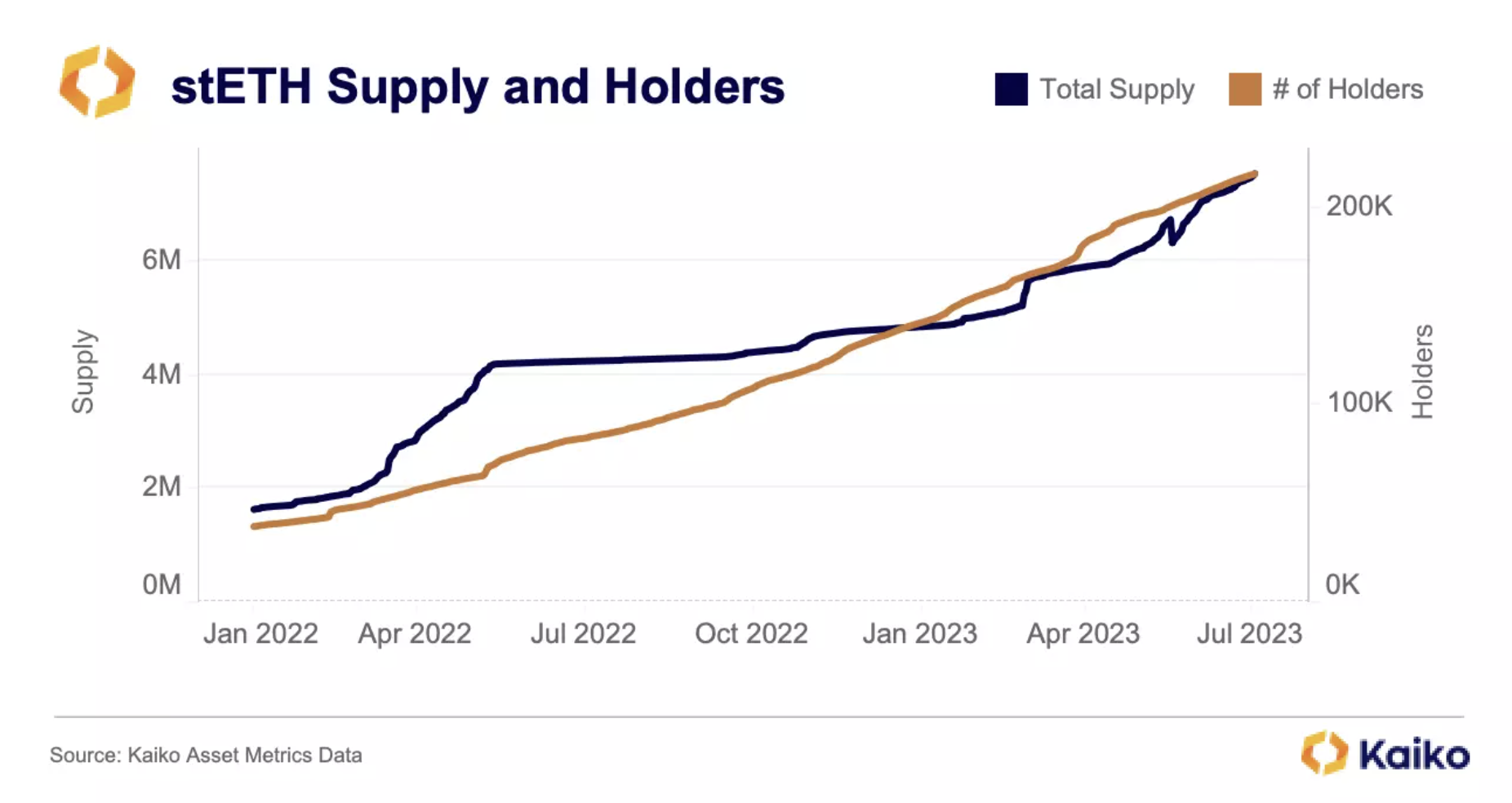

Lido Finance is a platform that allows users to stake Ethereum and receive stETH tokens, which represent the value of the initial deposit and staking rewards. Kaiko’s research reveals the impressive growth of stETH tokens over the past year and a half, with the supply increasing fivefold from 1.5 million to 7.5 million, and the number of holders rising from 40,000 to nearly 220,000.

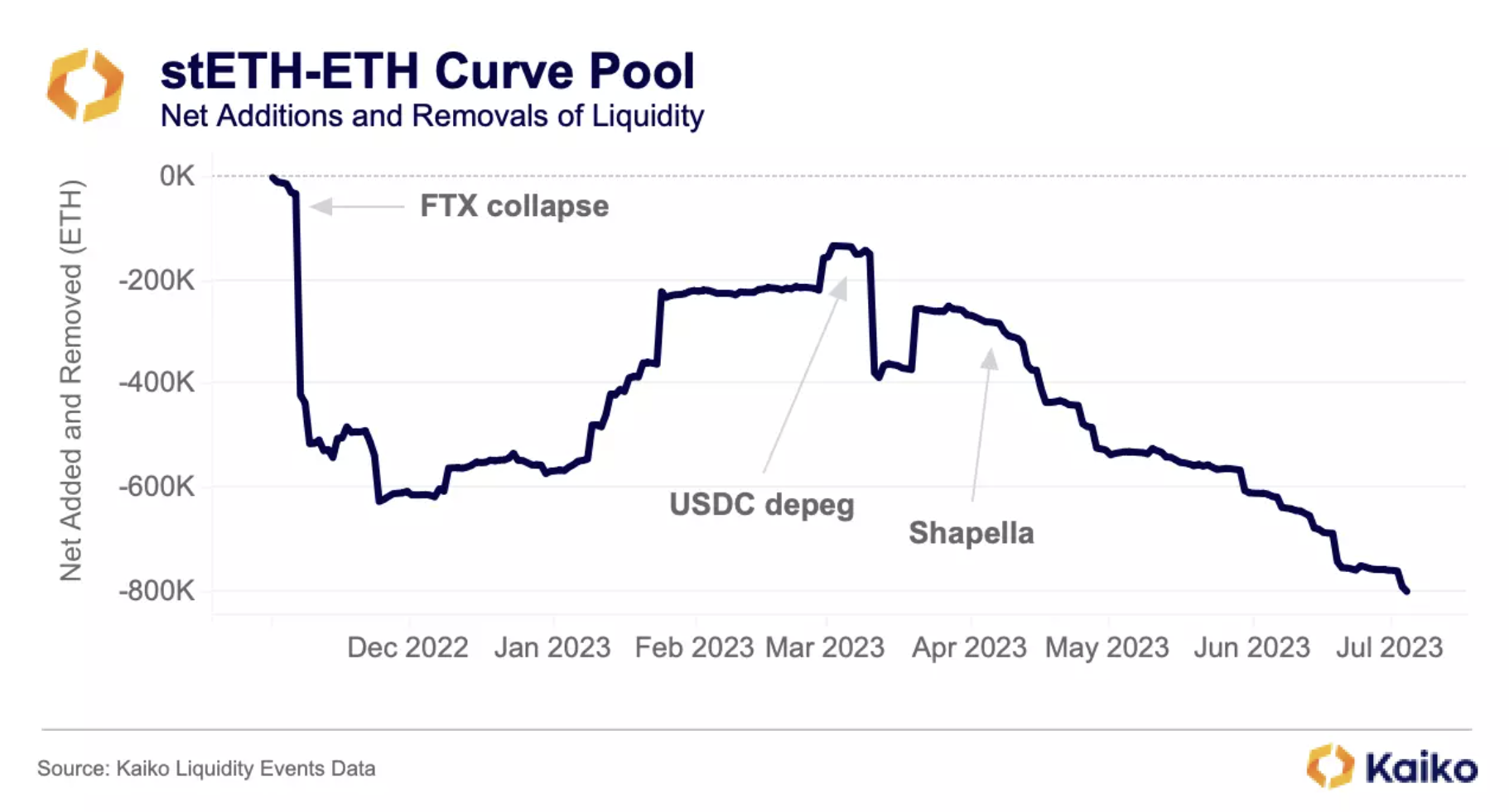

The analysis conducted by Kaiko also highlights the importance of liquidity in the context of staking derivatives like stETH. One crucial aspect emphasized by the research is Lido DAO’s reliance on Curve’s stETH-ETH pool for liquidity provision.

Kaiko’s data shows that since June 2023, liquidity incentives for this pool have been fading. As a result, liquidity has contracted, and a downward trend is evident. This change in incentives raises concerns about the stability of the stETH-ETH pool during periods of stress or market events, potentially triggering a liquidity crisis.

Another critical aspect explored by Kaiko’s research is the increasing leverage associated with stETH usage. The analysis points out that lending and borrowing protocols have become hubs for leverage, with stETH gaining popularity as an asset for leveraging strategies.

However, the research highlights the fundamental differences between stETH and ETH, coupled with deteriorating on-chain liquidity raises concerns about the risks associated with these leveraged positions.

Kaiko found that about one month after stETH was added to Aave V2 it became the most deposited asset, while ETH borrows skyrocketed from under $200mn to $1.6bn in just two months. The reason is alarming, according to the research firm:

This is in large part due to the popularity of manually leveraging stETH: depositing stETH into Aave, borrowing ETH, swapping or staking it for stETH, and repeating as many times as one is comfortable with. This is the process that starts to sound concerningly similar to 3AC’s GBTC trade, where the founders assumed that GBTC would trade closely with BTC.

Implications For The Future Of Ethereum And Lido

Based on the research, the combination of deteriorating liquidity and increasing leverage presents a precarious situation where a large liquidation event becomes more likely. Kaiko states:

Again, this is not a flaw in stETH but rather in how it is being used. In fact, any significant liquidation event that increases the stETH discount could present an incredible opportunity for anyone brave enough to catch the dip.

The data from Kaiko’s analysis reveals the withdrawal of liquidity from the stETH-ETH pool and emphasizes the potential risks arising from insufficient on- and off-chain liquidity.

This liquidity shortage could hinder the liquidation of substantial stETH positions, potentially burdening lending and borrowing protocols with significant bad debt.

Kaiko’s findings underscore the importance of caution, risk management, and proactive measures to address liquidity concerns in order to safeguard Lido’s future stability. In conclusion, the company has an advice for the Lido DAO:

The DAO understandably grew tired of providing such large incentives in the Curve pool, but with those incentives eliminated (for now) the DAO should seriously consider paying a market maker to provide liquidity on a variety of centralized and decentralized exchanges.

At press time, the LDO price plunged by 10% in the last 24 hours, trading at $1.90. The outlook for LDO currently looks extremely bearish as long as the price continues to move in the downtrend channel established in early March.