BlackRock CEO wants to move stocks and ETFs into crypto wallets after $150B success

BlackRock’s 2026 chairman’s letter positions the digital wallet as asset management’s next major distribution frontier.

In the letter, Larry Fink writes that “today, there’s very little access to traditional investment products in digital wallets” and that BlackRock plans to “lead the charge” in changing that.

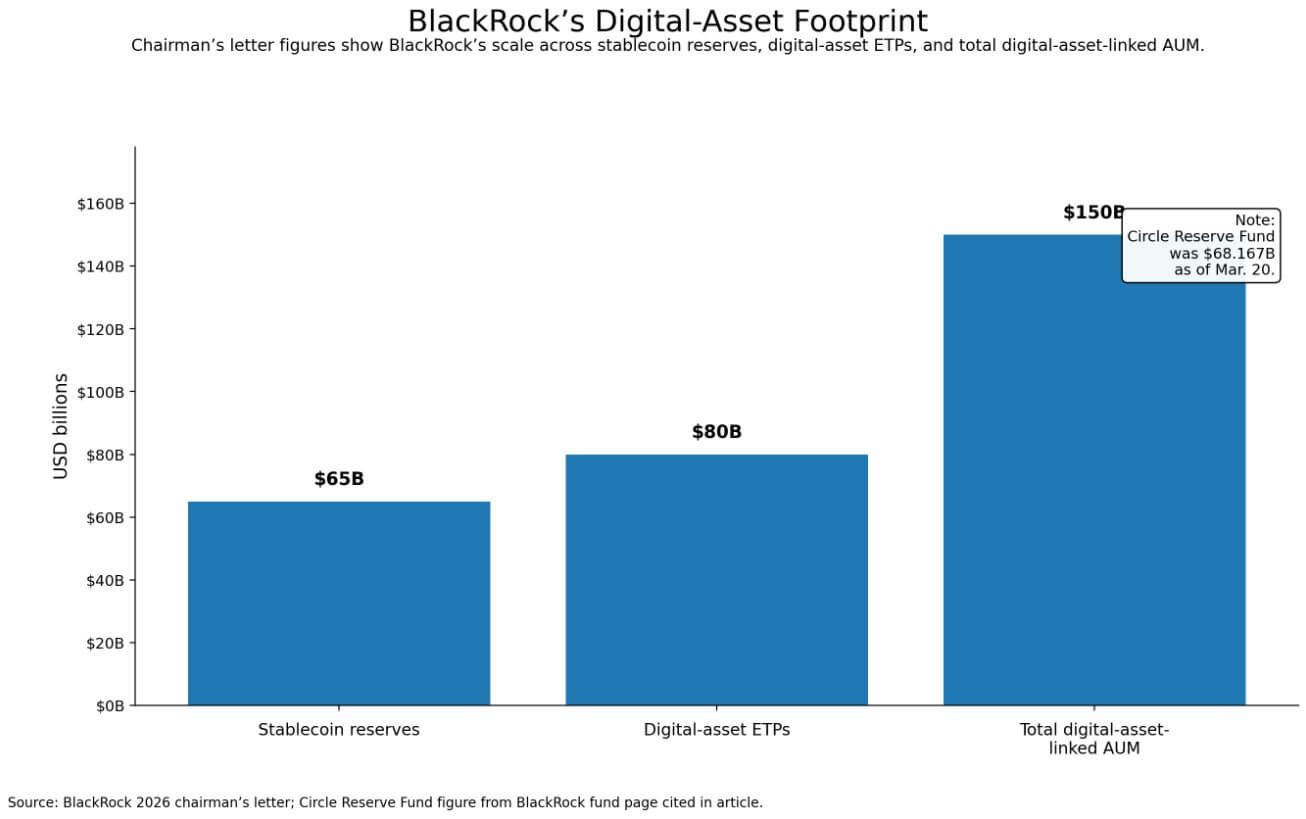

Numbers back the statement: BlackRock says it already has nearly $150 billion in AUM linked to digital assets, including $65 billion in stablecoin reserves and nearly $80 billion in digital asset ETPs.

Fink describes wallets as an underbuilt distribution channel for mainstream investing, one where BlackRock sees a structural gap and plans to move.

His vision is that a single regulated digital wallet could hold ETFs, digital euros, tokenized bonds, and fractional interests in assets like infrastructure and private credit.

From rhetoric to infrastructure

What gives this credibility is that BlackRock already operates across meaningful pieces of the stack.

The firm’s Circle Reserve Fund, which holds the majority of USDC’s reserve assets, stood at $68.167 billion as of Mar. 20, already above the $65 billion figure in the letter.

BlackRock’s BUIDL tokenized Treasury fund sat at over $2 billion as of Mar. 23, deployed across eight blockchain networks. Both are live, scaling positions with real AUM behind them.

In February, Uniswap Labs and Securitize announced that BUIDL would be tradable through UniswapX, with Securitize managing allowlisted investor access and compliance.

BlackRock’s head of digital assets, Robert Mitchnick, described it as a major step toward interoperability between tokenized dollar-yield funds and stablecoins.

The architecture is a BlackRock product exposure moving along crypto-native rails, cleared through a regulated compliance layer.

Fink connects the wallet argument to a broader distribution thesis developed elsewhere in the letter. He points to India, where JioBlackRock brought in more than a million investors in under a year, as a model for smartphone-native access to capital markets.

He writes that half the world already carries a digital wallet on their phone. The wallet passage reads as an extension of that logic, since the phone is already in the user’s hand, and the next step is to make financial products accessible through it.

RWA.xyz shows the tokenized US Treasury market at roughly $12 billion as of Mar. 23, with total stablecoin value at approximately $317 billion.

The on-chain cash layer and the tokenized asset layer are now large enough to function together as a distribution system.

Fink frames tokenization as an update to market plumbing, a way to make investments easier to issue, trade, and access across traditional and digital markets operating side by side.

That framing positions BlackRock’s wallet ambition inside a mainstream modernization story, and the firm’s own AUM figures back it up.

What the wallet thesis actually means

The most direct read of what wallet-native BlackRock products look like in practice starts with tokenized cash and Treasury exposure.

That is where the firm already has live scale and where the market already has traction.

Franklin Templeton’s Benji platform offers a concrete precedent. They offer a mobile application through which investors can buy, sell, and view tokenized fund positions, with yield distributed directly to their wallets and tokens transferable peer-to-peer.

The next layer is wallet-accessible ETF or fund share wrappers. Fink names ETFs explicitly as something a regulated digital wallet could carry.

BlackRock manages almost $80 billion in digital asset ETPs, giving it both the product infrastructure and the regulatory experience to extend that surface area toward wallet delivery.

Beyond that, the longer-dated path Fink sketches is fractional access to private markets, distributed through wallet interfaces to investors who currently reach those products only through advisers and high minimums.

| Product layer | What it could look like in a wallet | Why it is plausible |

|---|---|---|

| Tokenized cash / Treasury exposure | Wallet-accessible yield products, tokenized Treasury funds | BlackRock already has BUIDL and stablecoin-reserve scale |

| ETF / fund-share wrappers | Regulated wallet access to familiar public-market products | Fink explicitly names ETFs as something digital wallets could hold |

| Private-market exposure | Fractional interests in infrastructure or private credit | Fink explicitly points to tokenized private-market access as part of the end state |

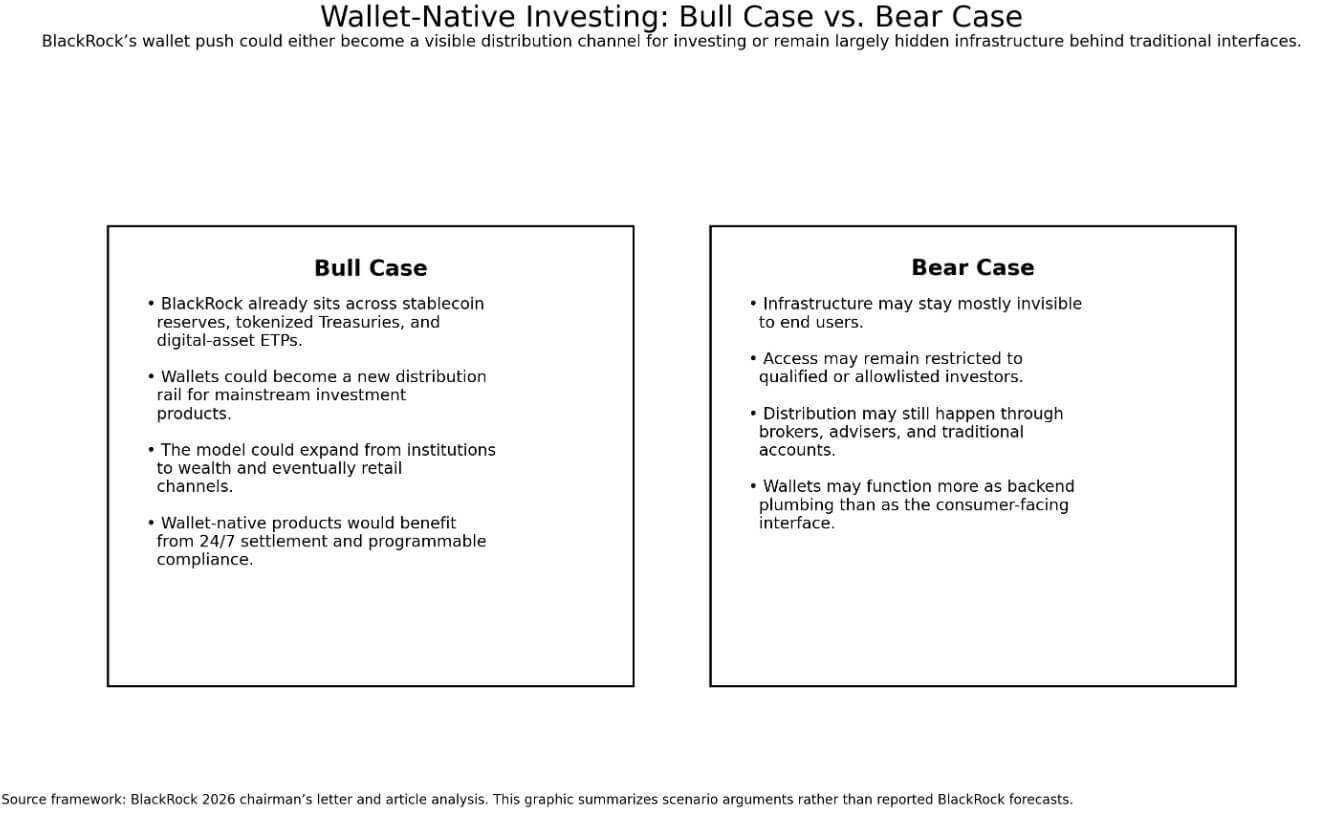

The bull case rests on the distribution scale, as BlackRock is already present at three points in the digital financial stack: backing the largest dollar stablecoin’s reserve, inside the largest tokenized Treasury fund, and managing the largest pool of digital asset ETPs.

If the firm uses that infrastructure as a foundation to push wallet-accessible products into wealth and, eventually, retail channels, it could accelerate the timeline for mainstream wallet-native investing.

Fink’s language around ETFs, private credit, and broader investor access points directly points down that path.

The bear case centers on infrastructure staying invisible to end users. BlackRock expands tokenization, settlement infrastructure, and stablecoin interoperability, but everyday investors continue to experience those improvements through brokers, advisers, and traditional account interfaces.

The current BUIDL structure points in that direction: US-qualified purchasers only, $5 million minimum, allowlisted access.

That is institutional plumbing running on on-chain architecture, still well upstream of a consumer distribution product.

The letter emphasizes modernization and coexistence with traditional markets. The language is consistent with gradual infrastructure improvement.

What the letter does not resolve

The chairman’s letter leaves the most operationally specific questions open.

There is no launch date, no named wallet product, no specified blockchain rail, and no clear statement on whether BlackRock’s wallet ambition targets institutional counterparties, wealth channel clients, or mass retail.

“Lead the charge” signals a strategic direction while the product details remain unannounced.

What the letter establishes is that BlackRock has moved from observing tokenization to operating within it at scale, and that Fink now sees the distribution gap in digital wallets as the firm’s next addressable problem.

Whether the product that closes that gap looks like a regulated tokenized Treasury wrapper accessible through a fintech partner or something closer to a self-custody investment account remains open.

The answer to this will likely define the next phase of BlackRock’s digital asset story.

If BlackRock succeeds in making wallets a distribution rail for traditional investment products, the competitive advantage of crypto-native infrastructure shifts toward settlement finality, programmable compliance, and 24/7 market access. These properties make wallet delivery of regulated products feasible in the first place.

The post BlackRock CEO wants to move stocks and ETFs into crypto wallets after $150B success appeared first on CryptoSlate.