The South Korean bank powering Upbit is testing Ripple integration for cross-border payments

South Korea’s Kbank has signed a strategic partnership with Ripple to test blockchain-based overseas remittances, placing a bank with a central role in Upbit’s KRW account access beside one of crypto’s longest-running payments infrastructure firms.

Local reports describe the work as a technical verification, or proof-of-concept, focused on whether Ripple’s infrastructure can improve the speed, cost, and transparency of overseas remittances. ZDNet Korea separately described the test as part of a phased push around bank-linked overseas remittance infrastructure.

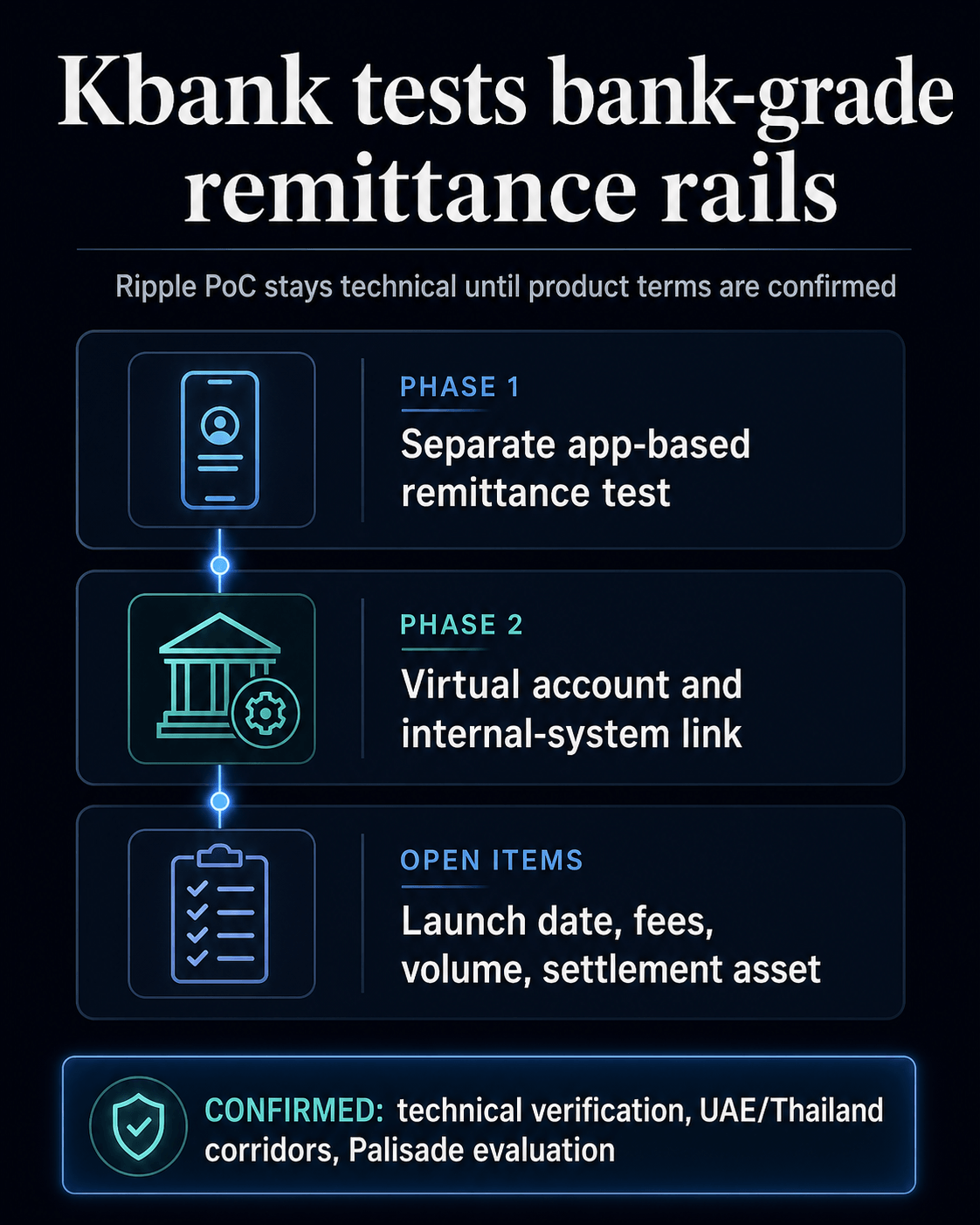

For now, the commercial pieces remain open: launch date, customer access, fees, live volume, and the exact settlement asset.

Kbank already sits inside South Korea’s crypto market through Upbit’s real-name account system. Its Ripple pilot, therefore, lands as more than a remittance experiment: it tests whether bank-side crypto infrastructure can move from exchange access toward ordinary cross-border payments while the product design and rulebook remain unfinished.

What Kbank and Ripple are testing

The Kbank-Ripple agreement points to bank integration rather than a standalone crypto app. Local reports said Kbank CEO Choi Woo-hyung and Ripple APAC head Fiona Murray attended a signing ceremony at Kbank’s Seoul headquarters, with the companies discussing a Ripple digital-wallet proof-of-concept, support for Kbank’s overseas remittance model, and broader digital-asset cooperation.

The sequence starts with a separate app-based remittance structure. The next step virtually links customer accounts and internal systems to test remittance stability, checking whether blockchain remittance rails can be mapped onto account and operations layers that resemble the systems a regulated bank would actually use.

That second phase also reportedly tests on-chain transfers involving corridors such as the UAE and Thailand. The corridor detail makes the PoC more operationally specific than a generic partnership announcement while keeping the commercial model open.

Palisade brings the wallet and custody layer into the test. Global Economic said the second phase uses or evaluates Ripple’s SaaS-based digital wallet Palisade, while Ripple’s own Palisade acquisition announcement describes the platform as wallet-as-a-service and custody tooling with features aimed at institutional digital-asset operations.

That makes the test a wallet and key-management exercise as much as a transfer-speed exercise. Production deployment by Kbank remains unannounced.

The technical focus is still meaningful. A bank remittance product has to solve compliance, custody, account linkage, settlement, and broader regulatory requirements. The PoC appears to test parts of that stack, while the full commercial design remains open.

Why Upbit changes the stakes

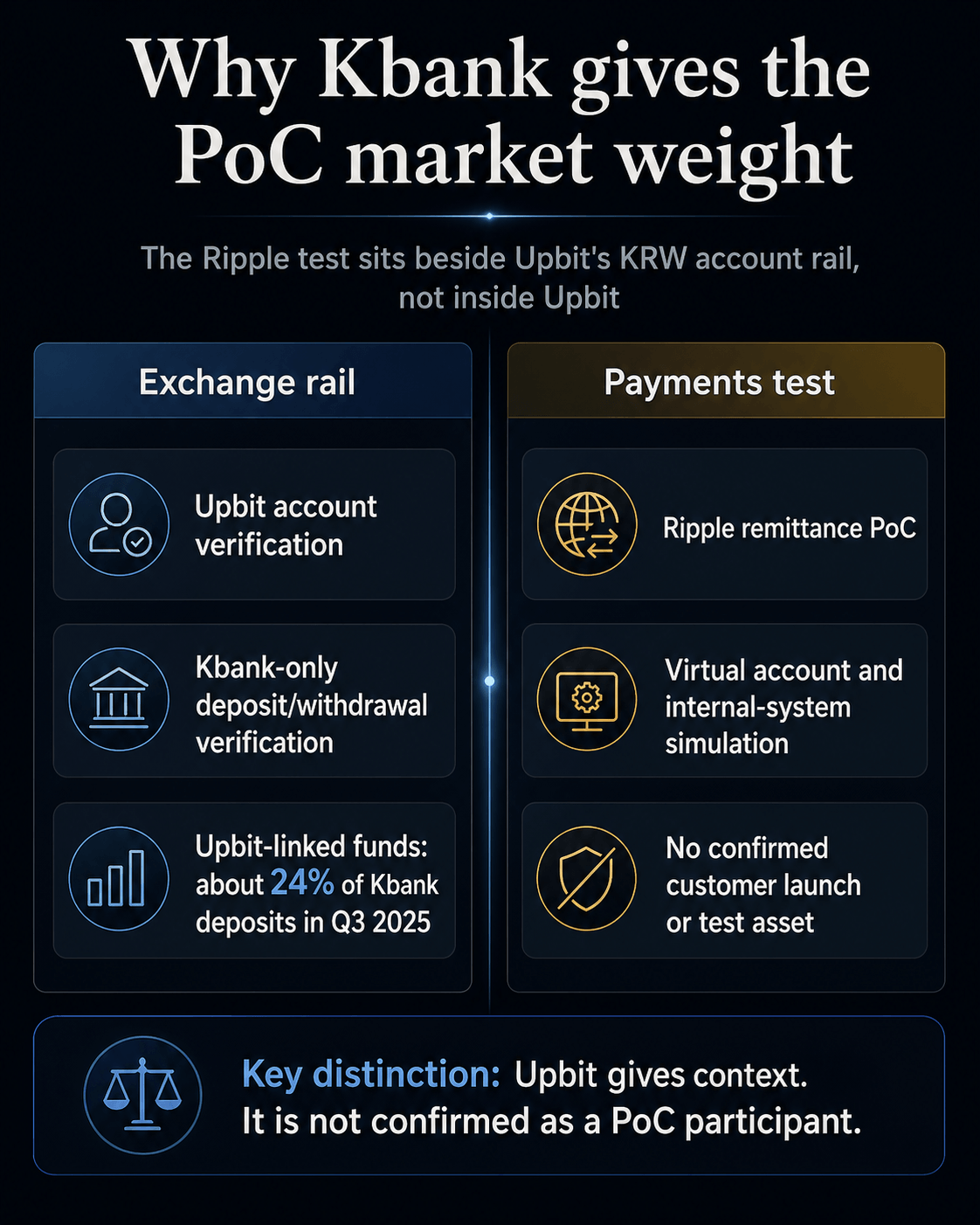

Kbank’s role in Upbit’s fiat access gives the Ripple test its market-structure relevance. The bank was moving to extend its real-name deposit and withdrawal account partnership with Upbit through October 2026, according to ChosunBiz.

Upbit’s own real-name account verification guide says deposit and withdrawal account verification is possible only with Kbank.

Taken together, the partnership report and Upbit’s guide make Kbank the bank behind Upbit’s KRW real-name deposit and withdrawal account verification rail. They do not show Upbit participating in the Ripple PoC or Kbank running the test on Upbit’s behalf.

The size of the Upbit relationship explains why the context has force. Upbit-linked funds accounted for about 24% of Kbank’s 30.4 trillion won deposit balance as of the third quarter of 2025, according to Korea JoongAng Daily.

The same report quoted Choi discussing Kbank’s need to reduce reliance on Upbit while positioning stablecoins and cross-border payments as future opportunities.

Kbank’s crypto-linked banking role has been built around exchange access. The Ripple test examines whether similar bank-side plumbing can be used for payments.

The first use case is account access for trading. The next possible use case is cross-border money movement. Between those two sits the unresolved question of regulation.

That context should not be stretched into Upbit participation. Upbit explains why Kbank’s banking role matters to South Korea’s crypto rails; the Ripple agreement remains a Kbank-side remittance PoC.

CryptoSlate’s prior coverage helps define the surrounding terrain. A June 2025 article covered South Korean banks pursuing a won-backed stablecoin push, while an April 2026 CryptoSlate report on Ripple’s RLUSD in Japan showed how bank trust can shape Asian stablecoin adoption.

Regulation keeps the test provisional

South Korea’s bank-led stablecoin debate gives the remittance test a policy edge. The Kbank pilot is already being tied to South Korea’s stablecoin rulemaking debate, while Seoul Economic Daily reported that delayed digital-asset legislation has kept some Korean blockchain and remittance infrastructure from moving into actual operations.

Banks can test the mechanics before they know the final rulebook. They can examine wallet architecture, account linkage, compliance controls, and cross-border flows. They can also build optionality without committing to a product launch.

Note: Kbank, the South Korean internet-only bank in the Ripple partnership, should be kept separate from Thailand’s KASIKORNBANK, often branded KBank.

KASIKORNBANK has appeared in related Korea-Thailand digital-asset remittance discussions, including a February cooperation announcement with Orbix and BPMG. The connection is corridor context and naming clarity, while the South Korean Kbank and Thailand’s KASIKORNBANK remain separate institutions.

The practical split is straightforward: what the pilot tests, what remains undecided, and why Kbank’s Upbit rail gives the work market weight.

| Confirmed | Still open | Operational implication |

|---|---|---|

| Kbank and Ripple signed a strategic partnership for remittance technical verification. | No production launch date or customer rollout has been confirmed. | The work remains a bank-side PoC before customer rollout. |

| The current phase virtually links customer accounts and internal systems and tests UAE/Thailand on-chain transfers. | The exact settlement asset, fee model, and live transaction volume remain undisclosed. | The test targets bank integration, but the commercial model is still undefined. |

| Upbit account verification for deposits and withdrawals is available only with Kbank, according to Upbit’s guide. | Upbit has not been identified as a participant in the Ripple PoC. | Kbank’s exchange-rail position gives the test relevance while exchange integration remains unsupported. |

| South Korea is still working through stablecoin and digital-asset payment rules. | The final rule set for bank-led digital remittances remains unsettled. | Regulation is a key gate between technical readiness and commercial launch. |

The next test is commercial proof

Kbank is now sitting between two roles. One is already visible: banking access for Upbit’s KRW deposit and withdrawal verification.

The other is being tested: blockchain-based overseas remittances that connect with bank accounts and internal systems.

That bridge has strategic value because South Korea’s crypto market already depends on tightly controlled bank-account rails. If a bank tied to those rails can also make blockchain remittances operational, the boundary between exchange access and payment infrastructure becomes less fixed.

The same compliance-heavy banking layer could become a place where crypto-linked infrastructure moves from trading access into cross-border money movement.

For now, the PoC covers testing, corridors, account-system simulation, and Palisade evaluation. It does not yet provide the commercial pieces that would turn the work into a live remittance business.

The next threshold is concrete: a named product, a live customer flow, a settlement asset, a fee model, and regulatory clearance.

Until those pieces arrive, Kbank’s Ripple partnership is best read as a readiness test with unusually important surroundings. It shows that one of South Korea’s key crypto-linked banking rails is examining the payments infrastructure.

It also shows how much still depends on regulation before a technical pilot can become a real remittance business.

The post The South Korean bank powering Upbit is testing Ripple integration for cross-border payments appeared first on CryptoSlate.